Many active fund managers are feeling beleaguered. Media consensus nearly unanimously guides investor toward passively managed ETFs and funds and decry the shortcomings of active management.

It is no wonder. Passive funds have largely outperformed passive funds for 10 years running[i]. Mutual fund cash flows have favored passive funds as well. What’s an active fund manager to do?

One lesson we’ve learned over years of watching investor behavior is that when everyone is moving in the same direction, it is usually a good idea to question it. A new research report from Leuthold Group provides a glimmer of hope for active managers. Said Leuthold Director of Equities Scott Opsal about the widespread belief that passive will become the dominant style forever, “We disagree, and believe that the active/passive relationship has been, and always will be, cyclical.”

Adds Opsal, “In a rip-roaring bull market, the most profitable strategy is to close your eyes, hold on tight, don’t think too much, and ride the trend for all it’s worth. Passive investing is the ideal vehicle in this situation. But in rotating markets that are grinding slowly higher, in high risk and uncertain environments, and especially in bear markets where losing money becomes the ultimate concern, the wisdom, experience, and discretion provided by skilled active managers become valuable attributes.”

Those who believe our 8-year-old bull market will go on forever may disagree with Opsal. But many active manager can take heart. When communicating through this challenging environment in investor letters, sales decks or thought leadership pieces, we encourage active equity fund managers to remind existing and potential investors of the following:

- Diversification continues to be important. A well-diversified portfolio should include true style diversification. Having both active and passive funds makes sense as outperformance for each will be cyclical.

- Remind investors that the bull market will not go on forever and that active funds have historically outperformed in down markets. Opsal’s research found that a much higher proportion of active managers beat passive managers in volatile or down markets. Remind investors of how your approach has performed in a variety of market conditions.

- Describe how your investment approach differs from the index. Portfolio managers with high active share, meaning they are selecting investments that are decidedly different from the index, can make a strong argument that their performance will likely diverge from that of the index. This can be important for investors who fear following the index down in a market correction.

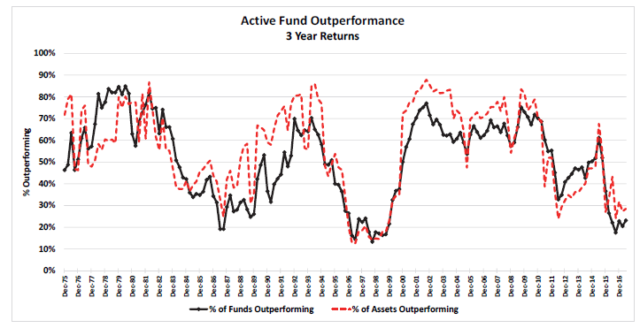

- Stress your performance over the long term. Active manager outperformance over longer time periods look decidedly better relative to passive performance. Consider the chart accompanying this post from Leuthold’s Opsal.

- Continue to clearly articulate your process, how your process works in a variety of market conditions, and why you believe your process makes sense in this market. What is it about how you pick stocks and what you are seeking to achieve will give investors confidence to stick with you into the future? And if you have underperformed of late, explain why and describe why you continue to believe your approach is the right one to take. For more perspective on this point, read our post titled “Consistently Emphasizing Process Helps Active Managers Maintain Media Credibility during Down Periods.”

- If you are a bond or international manager, remind investors that many of these approaches have consistently outperformed indexes. According to a recent paper from Chautauqua Capital Management, 74% of Foreign Large Blend actively managed funds outperform the index over five years. A majority of active bond managers also consistently outperform their passive brethren. The active/passive debate for stocks is really focused on US Stocks. For that matter, one could even argue it is mostly about large cap US stocks.

We appreciate the recent frustrations active managers face. Continuing to communicate the advantages of your actively managed approach should ultimately pay off when markets go through their inevitable cycles.

[i] S&P Dow Jones Indices “SPIVA® Institutional Scorecard: How Much Do Fees Affect the Active Versus Passive Debate?” August 8, 2017